Longboat Key Condo Financing: What Buyers Should Know

Danielle Gladding & Alison Kanter January 1, 2026

Danielle Gladding & Alison Kanter January 1, 2026

By Danielle Gladding & Alison Kanter | Danielle Gladding & Co. Realty | Bay Isles Resident, Queens Harbour

Shopping for a condo on Longboat Key can feel like learning a new language. Listings talk about months of supply, special assessments, warrantable projects, and flood zones — and it is not always clear what actually matters when you have to live with the decision.

I am Danielle Gladding. I have lived on Longboat Key since the late 1970s, I have been a licensed Broker since 1987, and I live in Queens Harbour inside Bay Isles. I walk these streets every morning, greeting neighbors and their dogs. My daughter Alison Kanter and I work together as a mother-daughter team at Danielle Gladding & Co. Realty — two generations of Sarasota knowledge, with no agenda except finding you the right home.

This is the guide we wish every buyer had before their first showing. Before we look at a single listing, let us talk about how to read this market — honestly.

“There is waterfront, and then there is the right waterfront for you.” — Danielle Gladding

A few core numbers tell you almost everything you need to know about a building, a submarket, and where the leverage sits today.

• Active inventory — how many condos are for sale right now. Low inventory favors sellers; rising inventory gives buyers room.

• New listings vs. pendings — new listings show supply coming in; pendings show real-time demand.

• Months of supply — how long current inventory would take to sell at today’s pace. This tells you who has the negotiating edge.

• Median sale price and price per square foot — median reduces outlier effects; price per square foot lets you compare apples to apples.

• Days on market and list-to-sale ratio — DOM shows how quickly units go under contract; list-to-sale ratio reveals real negotiation pressure.

• Inventory by property type — on Longboat Key, waterfront vs. non-waterfront and high-rise vs. low-rise matter more than almost anywhere else.

Longboat Key is an island market with smaller sample sizes and strong seasonal swings. A few high-priced waterfront closings can move the median in a single month. That is why a snapshot lies — and why Alison and I always run the numbers across the last 90 days and the last 12 months, in the same building or immediate area.

For clearer comparisons, look at:

• North Longboat (closer to Manatee County services)

• Central Longboat

• South Longboat — including Bay Isles on Longboat Key (closer to Sarasota)

Then separate waterfront from non-waterfront, and high-rise from low-rise. Finally, confirm whether the property sits in Manatee County or Sarasota County — taxes, appraiser records, and some permitting items differ by county. Longboat Key spans both.

From late fall through early spring, seasonal residents and out-of-state buyers arrive. Showings pick up. Well-positioned listings move quickly. You see more inventory — and more competition.

From late spring through fall, activity slows. Days on market often stretch. Some sellers are more open to negotiation — and a patient buyer with very specific criteria can do well. The tradeoff is fewer new listings, so the right unit may simply not be on the market yet.

A short DOM in mid-winter usually signals strong demand for that unit or building. A quick sale in summer can be an outlier. Compare DOM to recent closings in the same building or immediate area — not to island-wide averages, which on a small island like ours can be misleading.

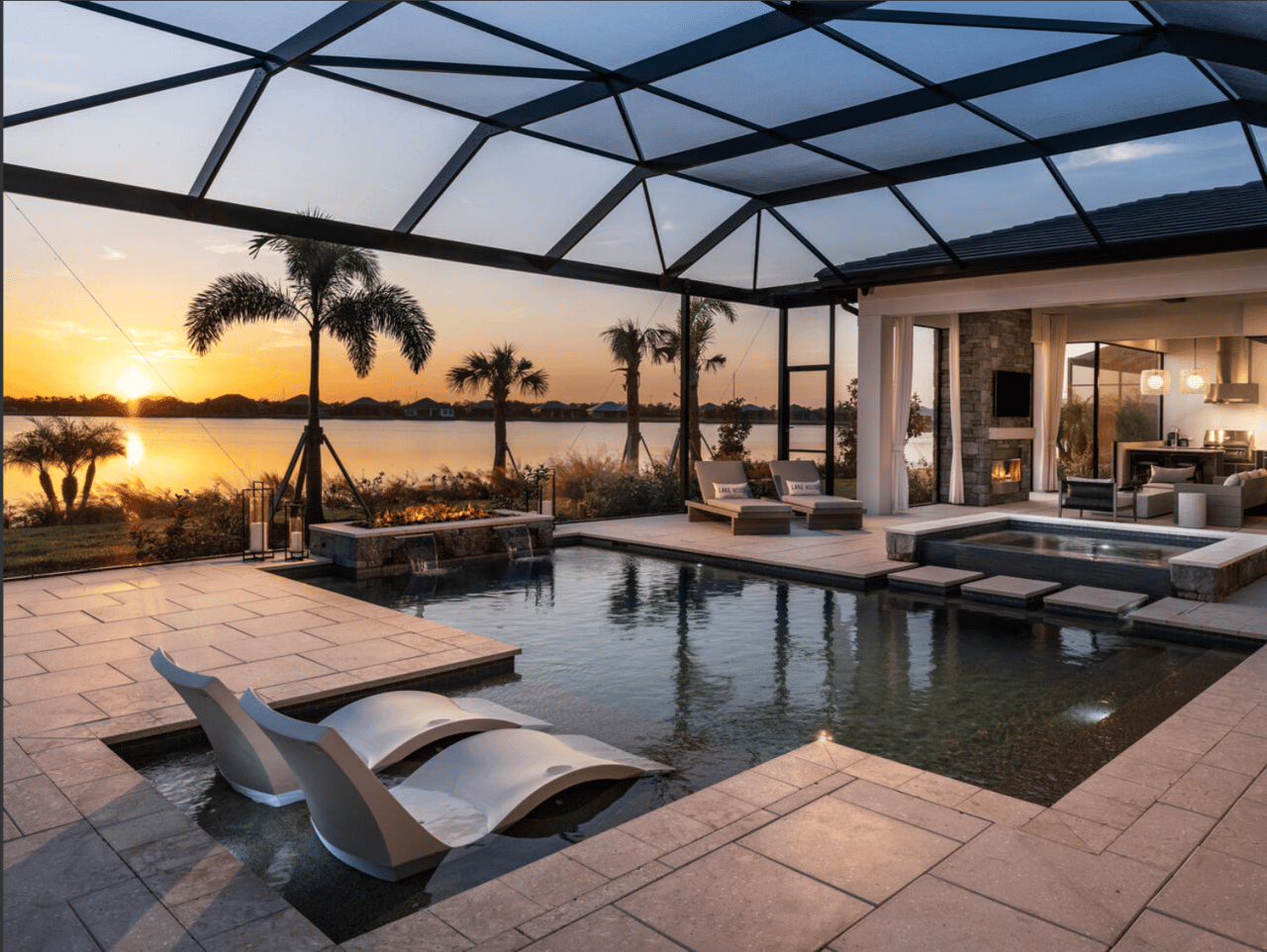

Waterfront is the biggest single value driver on Longboat Key. It also comes with the most expensive mistakes if you do not understand what you are buying.

Waterfront condos command higher prices for views, deeded or private beach access, boating access, and scarcity. The size of the premium depends on direct water exposure, view corridors, dockage, building quality, and amenities — elevator access, covered parking, pool, and hurricane protection.

Here is something I tell every Bay Isles buyer: in our community, every resident has deeded access to the private Bay Isles Beach Club on the Gulf of Mexico. You can live on the bay side — more privacy, better value — and the Gulf beach is still yours by deed. That is the kind of structural advantage the smartest buyers in this market already know.

• Insurance — Florida waterfront premiums have been climbing. Pull a quote from a local agent before you remove contingencies.

• HOA fees and reserves — coastal buildings carry more maintenance (seawalls, docks, corrosion control). Reserve funding levels affect future assessments and financing.

• Special assessments — look for anything planned or recent tied to capital projects. Get it in writing.

• Flood zone and elevation — verify both. First-floor height and building elevation change your insurance and your peace of mind.

• Seawalls and erosion — condition, permits, and repair history.

• Building age and structure — older waterfront buildings may need balcony, concrete, or envelope work. Ask for recent inspection reports and scopes.

• Dock ownership — deeded or common? What are the transfer rules and maintenance obligations?

Waterfront condos can show strong rent potential in high season, but often face tighter association rules and higher insurance and maintenance. In storm events or insurance market shifts, waterfront values can behave differently than interior units. Scarcity supports recovery in stable periods — but you need to model holding costs honestly. As a fellow investor for decades, I think about every property the same way you do: what does this really pencil out to?

Longboat Key spans Manatee and Sarasota counties. Confirm the parcel’s county on day one so you can review the correct property appraiser and tax history. Some permitting and exemptions differ.

Ask for these as early as possible:

• Current budget, last reserve study, and audited financials or treasurer’s report

• Past 12–24 months of meeting minutes

• Declaration / CC&Rs, bylaws, and house rules

• Rental rules and any short-term rental restrictions

• Master insurance policy declarations and certificates

• Pending or proposed special assessments

• Any litigation disclosures

These documents can reveal reserve gaps, future capital needs, rental limits, or litigation that affects financing and resale. We help our clients read them line by line — and tell you what we would tell our best friend, including the things that might give you pause.

• Warrantable vs. non-warrantable — lenders look at reserves, insurance, owner-occupancy ratios. Non-warrantable projects often require larger down payments or cash.

• Loan types — FHA and VA maintain project approval lists. Conventional financing may still be available, but underwriting is stricter on barrier islands.

• Second-home underwriting — lenders treat second homes differently than primary residences. Confirm guidelines for your unit size, occupancy, and building type before you write an offer.

Expect to discuss homeowners coverage, wind or hurricane coverage, and flood insurance. Elevation, prior claims, and building construction all matter. Build conservative insurance estimates into your budget and verify with a local agent before you remove contingencies — not after.

Town regulations and HOA rules both apply, and HOAs are often stricter than the town. Confirm minimum rental periods, annual caps, and required registrations or taxes. If rental income is part of your plan, model winter and shoulder-season occupancy separately — do not blend them.

Use a licensed inspector and consider a structural engineer for older waterfront buildings. Focus on balconies and terraces, concrete and slab integrity, waterproofing, pool and mechanical systems, roof, windows and doors, and hurricane protection. Ask the association for any recent engineering reports, scopes of work, or completion documents.

• Confirm county (Manatee or Sarasota) and pull property tax history

• Request the full HOA package and study reserves, insurance, and minutes

• Get lender pre-approval that addresses condo underwriting

• Verify rental rules if you plan to rent seasonally

• Price insurance with a local agent — including flood

• Book inspections and add structural review if waterfront

• Compare comps in the same building and immediate area first

Listing ahead of peak season can capture early demand. Listing in season taps the widest buyer pool. Either path can work — what matters is a focused pricing strategy and a clean, lifestyle-led presentation. Alison and I watch new listings, pendings, and DOM in your building and the nearby buildings to fine-tune as we go.

Share known material facts — building projects, special assessments, association issues. Buyers and lenders are looking. Clear documentation speeds underwriting and protects your contract.

Have HOA contact details, current statements, and recent insurance or utility invoices ready. If your association recently completed work, keep the report and proof of completion on hand. A clean package reduces timeline risk during the busy season.

• Sarasota / Manatee MLS reports for active, pending, and closed sales

• Town of Longboat Key for ordinances, building, and rental rules

• Manatee County and Sarasota County Property Appraisers for parcel and tax history

• County Clerk / Records for recorded declarations and amendments

• FEMA and NOAA for flood and sea-level tools

• Florida Office of Insurance Regulation and local insurance agents for current market conditions

When you review any listing, confirm: is it waterfront? Building age and recent capital projects? Current monthly assessment and coverage? Pending special assessments? Rental rules? Flood zone and elevation? Recent comparable sales in the same building?

My job is not to sell you a condo. It is to help you choose the right one — for your lifestyle, your family, and your future. Alison and I bring two generations of Sarasota knowledge, deep neighborhood expertise across Longboat Key’s waterfront and luxury condo communities, and a boutique experience with the reach of an institutional brand.

We live here. We know this community like no one else. Let us help you do this honestly — and well.

Schedule a Free Consultation with Danielle & Alison

DanielleGladdingCo.com · Danielle Gladding & Co. Realty · Bay Isles, Longboat Key, FL

Q: What is months of supply in the Longboat Key condo market?

A: Months of supply is how long current condo inventory would take to sell at the present sales pace. It helps you gauge whether buyers or sellers have leverage — and on a small island market like Longboat Key, it can shift faster than people expect.

Q: How does seasonality affect buying a condo on Longboat Key?

A: Activity rises from late fall through early spring, with more showings, more new listings, and faster sales. The off-season often brings slower velocity and more room to negotiate, but fewer options for very specific criteria.

Q: Which HOA documents should I request before buying a Longboat Key condo?

A: Ask for the current budget, last reserve study, audited financials, the past 12–24 months of meeting minutes, the declaration and house rules, master insurance certificates, rental policies, any litigation disclosures, and any pending or recent special assessments.

Q: How do flood zones affect condo insurance on Longboat Key?

A: Flood zone and elevation affect both insurance availability and price. First-floor height and building construction also influence insurability and premium levels — confirm both before removing contingencies.

Q: Are short-term rentals allowed in Longboat Key condos?

A: It depends. The Town of Longboat Key has its own regulations, and each association sets its own rental limits — which are often more restrictive than the Town. Verify minimum rental periods, annual caps, and registration requirements before assuming rental income.

Q: What makes a condo non-warrantable to lenders?

A: Common factors include low reserves, certain insurance issues, owner-occupancy ratios below lender thresholds, or pending litigation. Non-warrantable projects often require larger down payments or all-cash purchases.

Q: Should I compare condo prices island-wide or by building?

A: Start with recent sales in the same building or immediate area, then widen to similar buildings. Island-wide medians on Longboat Key can be skewed by a handful of high-end waterfront closings in a single month.

Q: When is the best time to list a Longboat Key condo for sale?

A: Listing just before or during peak season (late fall through early spring) captures the widest buyer pool. Early pre-season strategies can also work well if your pricing and presentation are aligned with current demand.

Q: Why work with Danielle Gladding & Alison Kanter for a Longboat Key condo purchase?

A: Danielle has been a licensed Broker since 1987 and lives in Queens Harbour inside Bay Isles on Longboat Key. Her daughter Alison Kanter joins her as a mother-daughter team at Danielle Gladding & Co. Realty — two generations of Sarasota expertise, deep neighborhood relationships, and honest guidance on every property.

Stay up to date on the latest real estate trends.

Lido Shores

They share a bridge, a zip code, and a way of life — but the buyer who belongs on Lido is not the buyer who belongs on St. Armands. Here’s how to tell the difference.

Buyer Education

Laurel Park and Towles Court are downtown Sarasota’s only true historic single-family districts — 1920s cottages a walk from Main Street, with real charm and real trad… Read more

Bay Isles

Corey's Landing is a gated enclave of sixty-one homes and patio villas inside Bay Isles on Longboat Key, with open-bay and golf-course residences, pool, tennis, and de… Read more

Florida Living

Country Club Shores or Bay Isles on Longboat Key? An honest comparison of deepwater single-family living vs gated community life, by Danielle & Alison.

Golden Gate Point

Harbor House West Sarasota: 226 Golden Gate Point Guide

Golden Gate Point

Harbor House at 174 Golden Gate Point — 13 owner-occupied residences, Sarasota Bay & Ringling Bridge views, boat dock, fishing pier. Alison Kanter & Danielle Gladding … Read more

Golden Gate Point

Harbor House South 400 Golden Gate Point — 13 units, bay views, boat docks. Danielle lived here. Alison Kanter & Danielle Gladding guide buyers & sellers.

Waterfront Condo

Older condos on Golden Gate Point can be the best value on the peninsula — the same walkable bayfront address for less per square foot — if the reserves and inspection… Read more

Lakewood Ranch

Lakewood Ranch is built for family life and top schools; the islands are built for the water and an adult lifestyle. The right Sarasota choice depends less on budget t… Read more

Lido Shores

Lido Shores is the densest concentration of Sarasota School of Architecture residences in the country — Paul Rudolph, Ralph Twitchell, the Umbrella House. Here is the … Read more

Why Queens Harbour on Longboat Key Offers a Lifestyle Few Communities Can Match

The Private Enclave Few Know About

Where Privacy, Nature, and Estate Living Meet on Longboat Key

A Local Perspective on Finding the Right Realtor for Longboat Key

Get assistance in determining current property value, crafting a competitive offer, writing and negotiating a contract, and much more. Contact Us today.